July 2023 East Bay Market Report

Market Update

Market Update

Note: You can find the charts & graphs for the Big Story at the end of the following section.

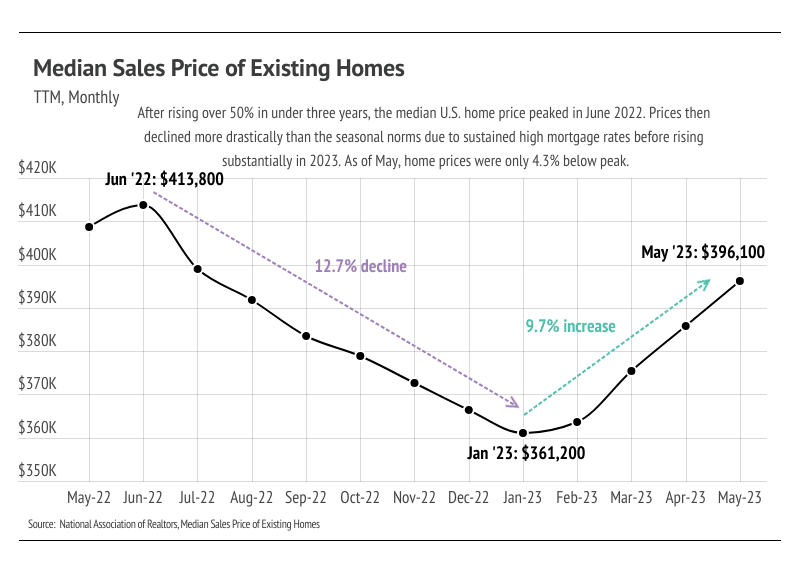

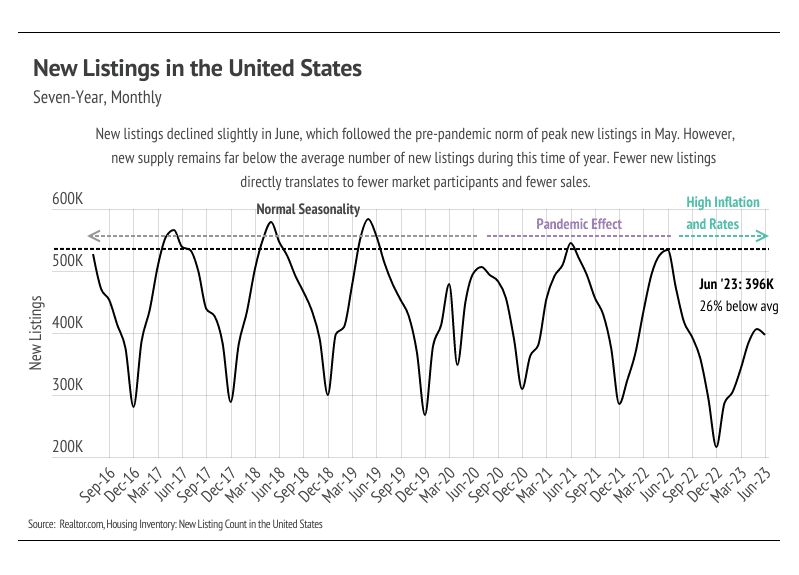

The median home price in the United States increased by slightly over 50% in less than three years from 2020 to 2022, peaking in June 2022 — the largest and fastest price growth in history. The dramatic rise in prices primarily resulted from pandemic-related stimulus and lifestyle changes, which incentivized buying a home that was worth spending considerably more time in. All of a sudden, homes became more valuable for buyers, but due to record-low mortgage rates, they also became more attainable, which led to a buying boom that caused inventory to hit record lows in February 2022.

At the same time, homeowners perfectly content with the homes they had also wanted to take advantage of the low mortgage rates, causing refinancing to skyrocket. Refinance rates reached their highest in history in the fourth quarter of 2020. Refinancing remained high in 2021 but fell slowly throughout the year. Generally, it doesn’t make financial sense to refinance, only to sell your property soon thereafter, because of the costs of the refi (often 2-6% of the loan). Between home purchases and refinancing from June 2020 to June 2022, the U.S. has an outsized number of homeowners who were able to lock in a mortgage rate at or near the lowest rate in history. Because most people don’t buy and sell or refinance homes year after year, the current inventory level is reasonable, albeit challenging for buyers.

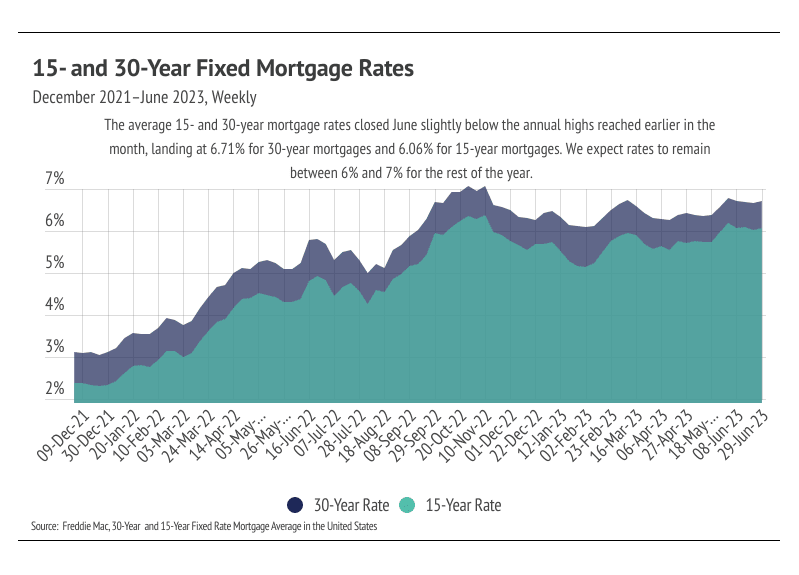

According to the National Association of Realtors (NAR), the median duration of homeownership in the United States was around 13 years in 2020. But let’s say, for the sake of example, we believe that number is no longer accurate, and it’s really more like five years. If five years is the median duration of homeownership, that means that pandemic-era buyers and refinancers likely won’t even start to consider reentering the housing market for at least another three years. It should be noted that five years is most likely generously low, particularly because the high mortgage rates (6.71% at the end of June) are disincentivizing homeowners who already have low rates from selling and buying a new home. As a result, low inventory is here to stay in most of the U.S., especially in highly developed areas where land for new housing is hard to come by. Additionally, mortgage rates will likely take three years to contract in a meaningful way as the Fed continues to raise rates in an effort to combat inflation.

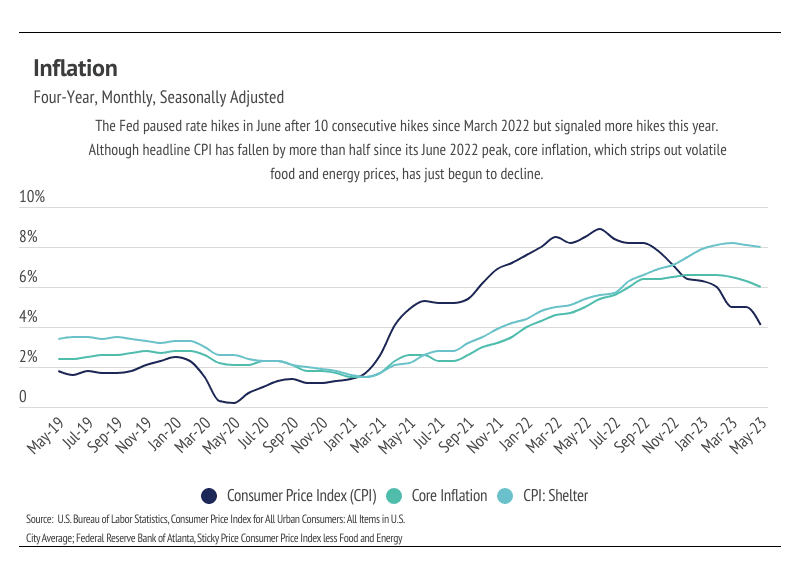

During the Fed’s June meeting, board members decided unanimously to pause rate hikes but noted that at least two more would likely occur this year. Although headline inflation (Consumer Price Index, or CPI) is down by half since it hit 9% last June, core inflation, which removes volatile food and energy prices from the inflation calculation, has barely started to fall. Core inflation peaked in December 2022 and has contracted 9%. A large component to core inflation is shelter. The Consumer Price Index for Shelter is only down 2% from the March 2023 peak. This isn’t exactly surprising. If we compare the monthly cost of financing a median-priced home with the average 30-year mortgage in December 2021 versus June 2023, the monthly cost has increased 95%.

Different regions and individual houses vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage for your area. In general, higher-priced regions (the West and Northeast) have been hit harder by mortgage rate hikes than less expensive markets (the South and Midwest) because of the absolute dollar cost of the rate hikes and the limited ability to build new homes. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

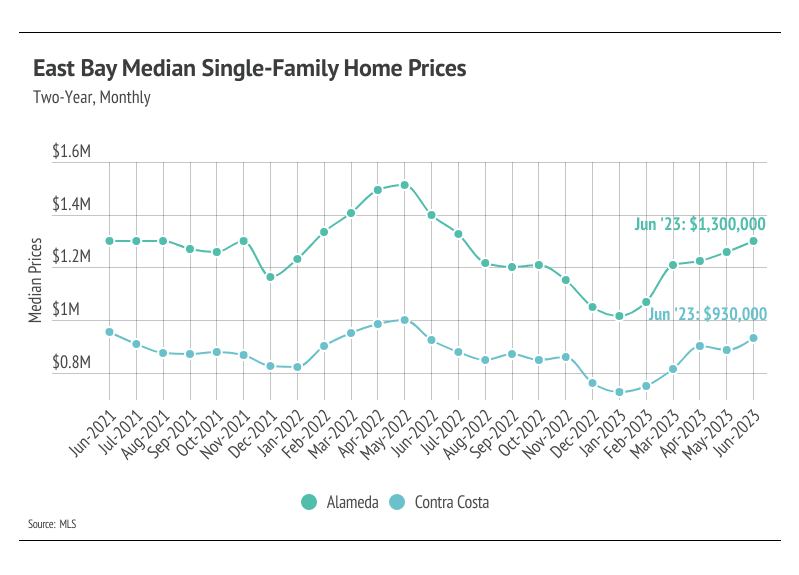

In the East Bay, the housing market is always experiencing high demand. Even as prices rise quickly in Alameda and Contra Costa, coupled with mortgage rates near 20-year highs, demand is still strong. High demand and low, but rising inventory are driving the rapid home price appreciation that the East Bay has experienced this year. Housing prices typically work in a counterintuitive way. In a classic supply/demand problem, as supply falls and demand remains steady or increases, prices rise. Housing works a bit differently. In the first half of the year, new listings usually rise rapidly, far outpacing sales and causing overall inventory to rise from the winter lows. Demand also tends to rise in the first half of the year, and the increasing supply actually benefits the overall market because buyers can more easily find a home that suits their wants and needs. Finding the right home is far more valuable than feeling forced into a home that’s not right, so prices tend to rise in the first half of the year.

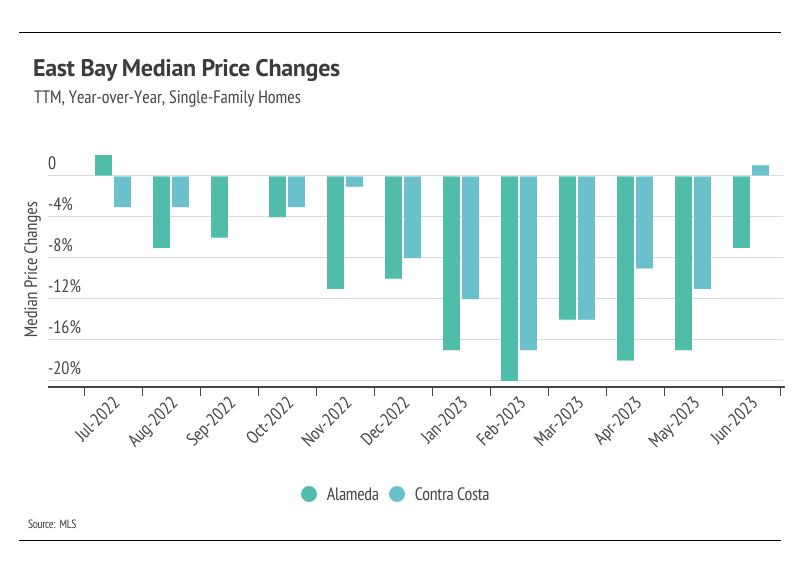

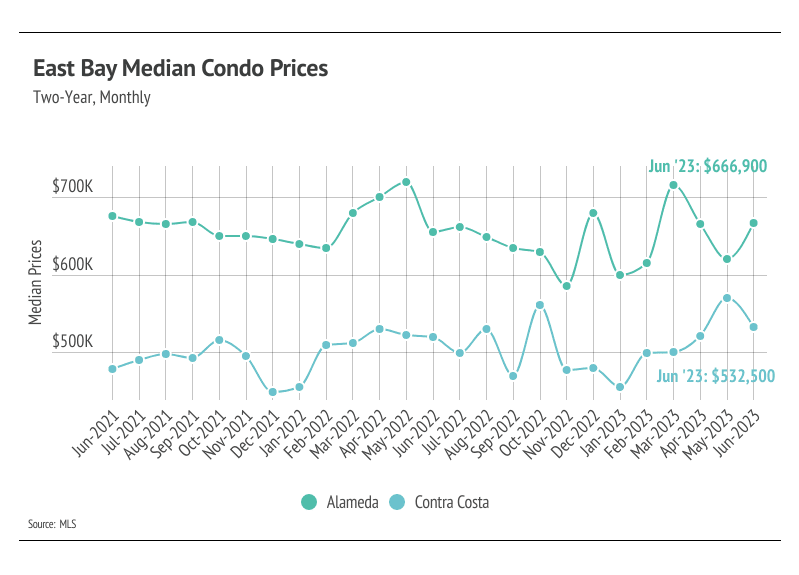

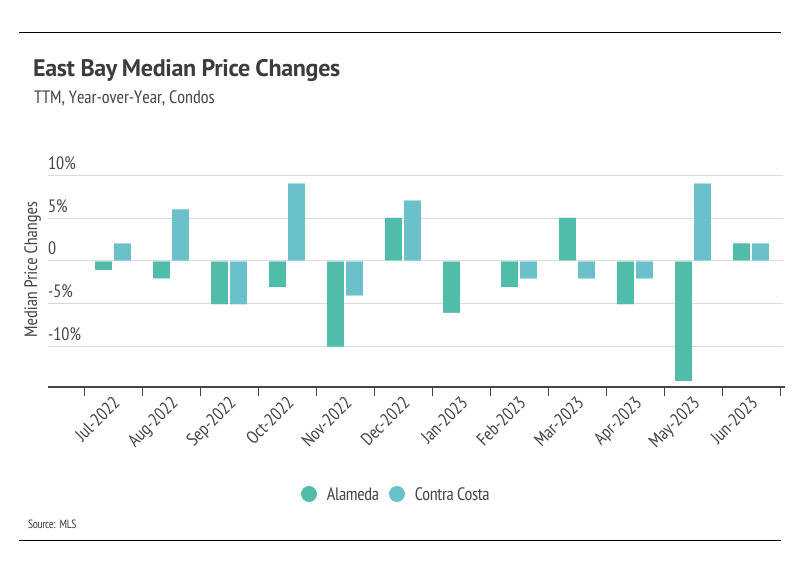

Year to date, single-family home prices have increased 24% in Alameda and 22% in Contra Costa. Condo prices in Contra Costa are up 10% in the first half of 2023, while Alameda condo prices are down 3%.

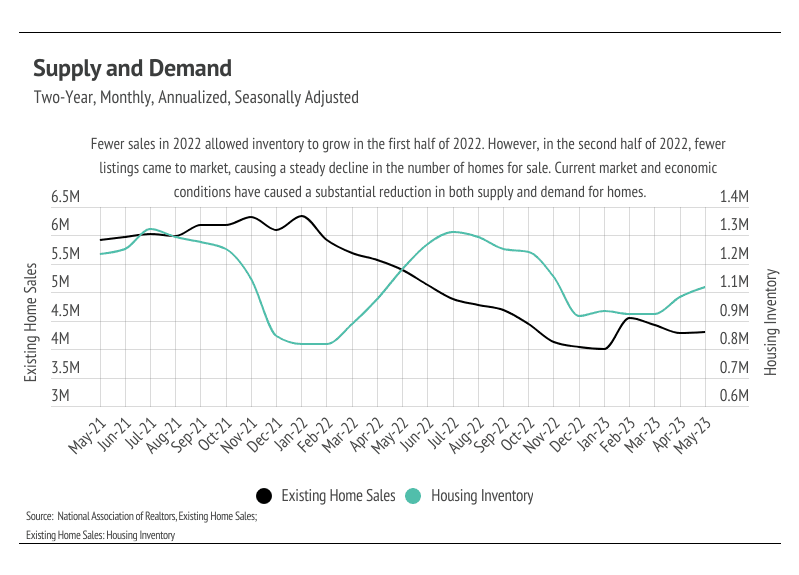

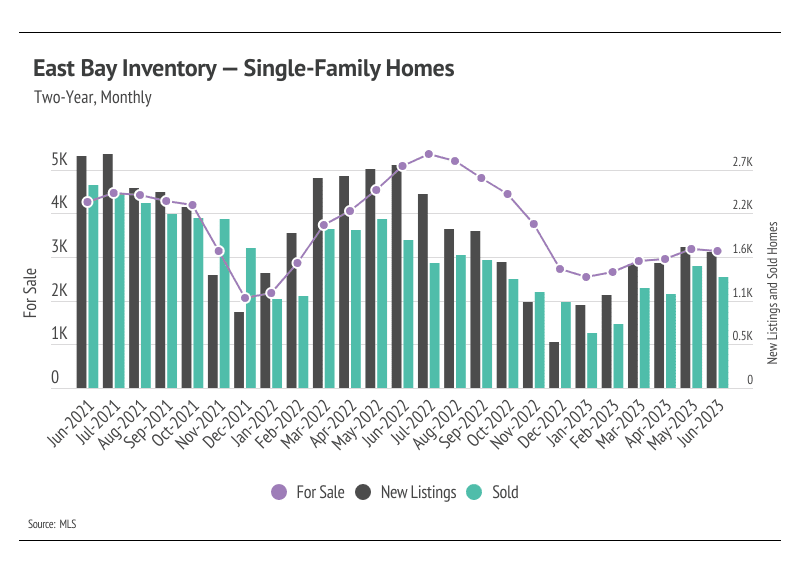

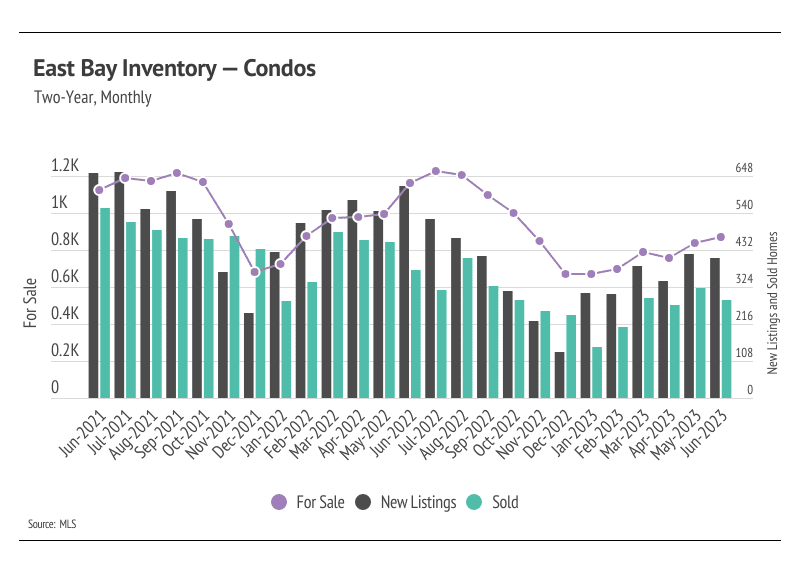

Single-family home and condo inventory, sales, and new listings rose in the first half of the year, although all remain at depressed levels. The number of home sales is, in part, a function of the number of active listings and new listings coming to market. Currently, inventory is so low relative to demand that any amount of new listings is good for the market. Potential sellers who have fully paid off their property are in a particularly good position if they don’t have to finance their next property after the sale of their home. Since January 2023, sales jumped 102% while new listings rose 57%, whereas last year, for example, sales rose 57% and new listings increased 82% in the first half of the year.

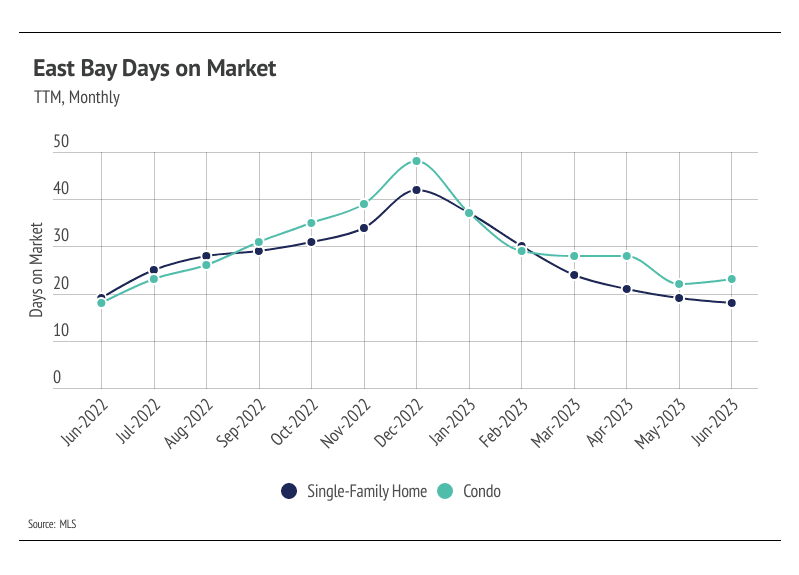

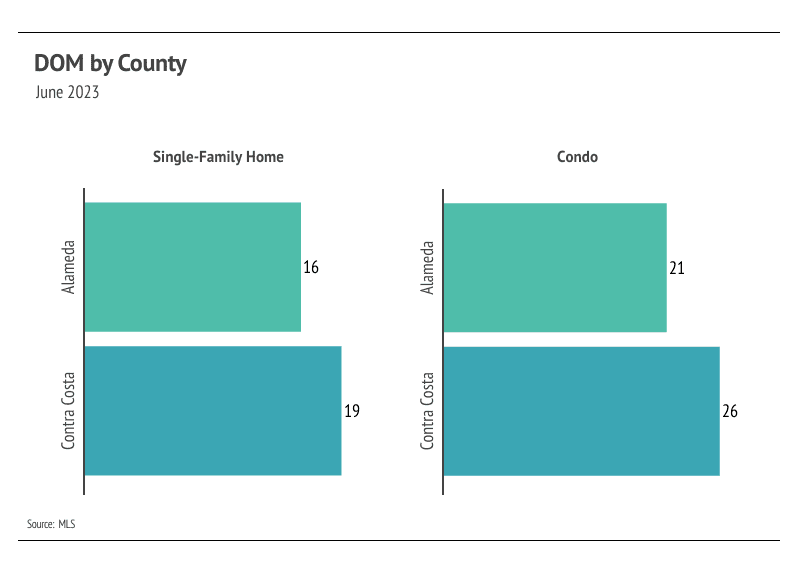

As buyer competition has ramped up and sellers are gaining negotiating power, sellers are receiving more of their listed price. In January 2023, the average seller received 95% of list price compared to 105% of list in June. Inventory will almost certainly remain historically low for the year, and the market will remain competitive in the third quarter.

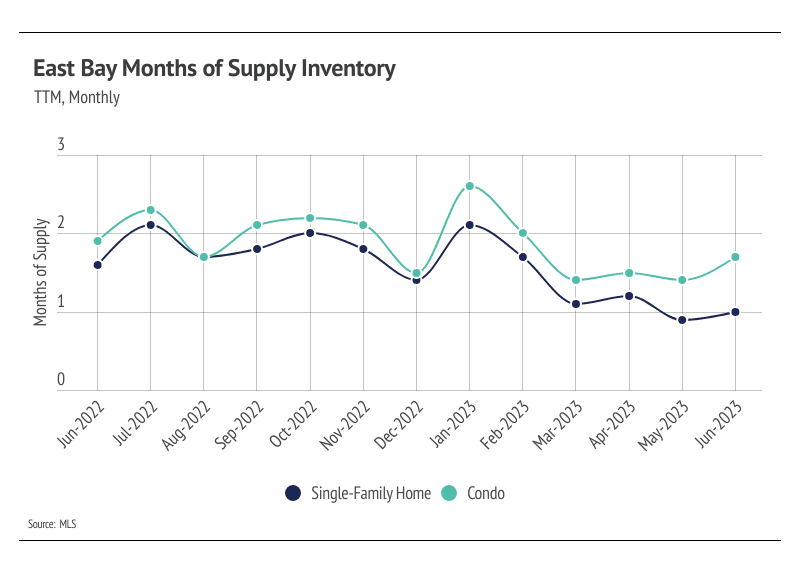

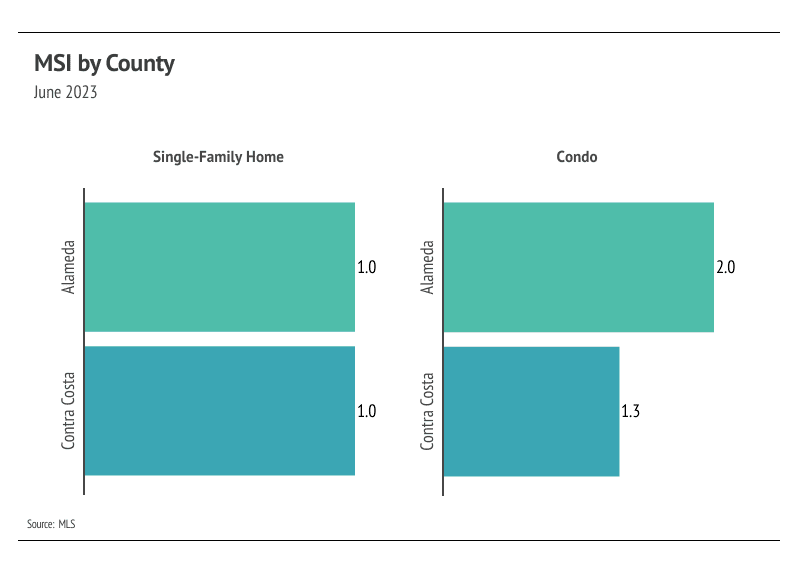

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). The East Bay market tends to favor sellers, which is reflected in its low MSI. MSI trended lower in the first half of the year for both single-family homes and condos, meaning the market more strongly favors sellers. The sharp drop in MSI occurred due to the higher proportion of sales relative to active listings and less time on the market.

Stay up to date on the latest real estate trends.

Tips For Your Home

Market Update

Real Estate

Tips For Your Home

Real Estate

Real Estate

Real Estate

Real Estate

Real Estate

You’ve got questions and we can’t wait to answer them.