May 2023 East Bay Market Report

Market Update

Market Update

Note: You can find the charts & graphs for the Big Story at the end of the following section.

While we navigate through the complexities of our current economic landscape, it's important to acknowledge that we find ourselves in a state of uncertainty. It's not quite accurate to label it a recession, but finding the perfect description for our economic condition can be challenging. Perhaps "economic limbo" resonates with some, while others prefer the term "uncertainty." One could even argue that "whiplash" captures the feeling of sudden shifts and unpredictability.

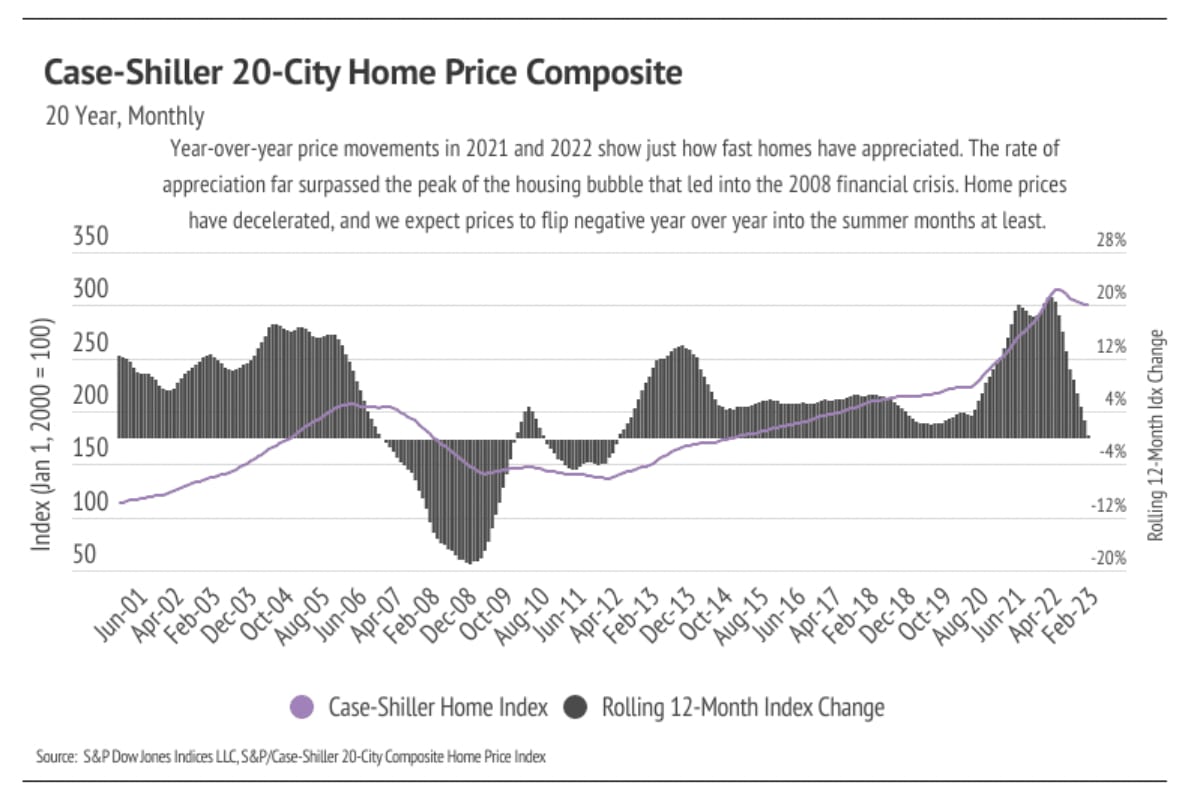

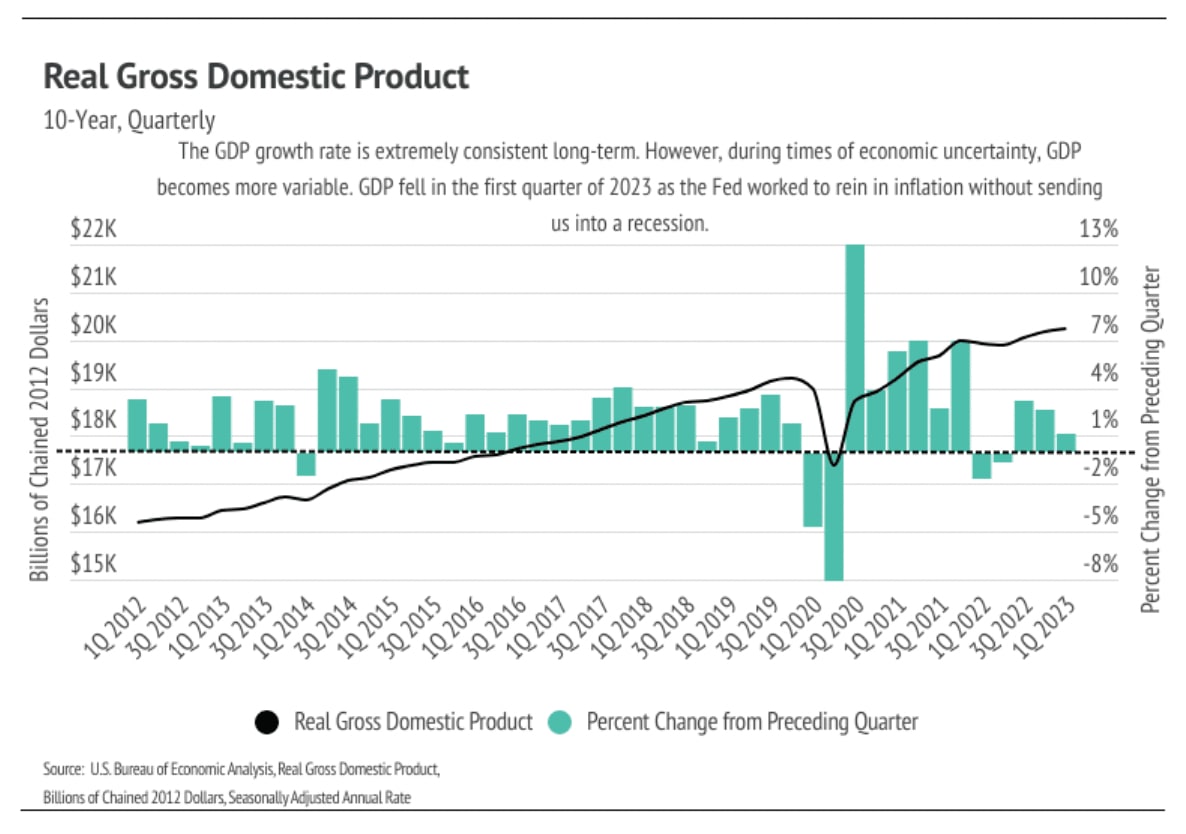

As we reflect on the past three years since the pandemic struck, it becomes evident that we are still grappling with understanding the dynamics of the pre-pandemic economy. It had flourished with such unwavering stability from 2012 to 2020 that envisioning a different reality seemed almost impossible. However, the pandemic's impact swiftly transformed our world, drastically narrowing down our options to a limited menu of activities: eating, working, buying, and sleeping - an ongoing cycle.

During this time, asset prices skyrocketed, and consumers found themselves with disposable income, eagerly seeking avenues to spend it. The availability of easy credit conditions further fueled price increases, particularly in the housing market, where prices surged. It's crucial to highlight the remarkable change in purchasing power experienced in 2020. Falling interest rates allowed prices to rise by up to 10% throughout the year while the monthly mortgage costs remained unaffected. To put it differently, a loan of $500,000 taken out in January 2020 had the same monthly payment as a $550,000 mortgage in December 2020. As we moved into 2021, interest rates remained consistently low, providing a measure of stability in an otherwise uncertain landscape.

In the dynamic real estate market of 2021, we witnessed an extraordinary number of buyers entering the scene, resulting in a surge of home sales that exceeded the long-term average by approximately a million. It was truly a remarkable time for the industry. However, as we look back, the rapid rise in inflation during that year served as a clear indicator that the era of easy monetary policy was coming to a close. This change had the opposite effect compared to the preceding years of 2020 and 2021.

Amidst these fluctuations, it is important to recognize that consumers felt a sense of affluence and, to a large extent, were indeed wealthier. With fewer options and opportunities to spend money, people naturally turned to saving, leading to an increase in overall wealth. The way we feel about our financial situation plays a significant role in making significant decisions. For many, if not most people, these feelings have undergone a shift, even if everything appears fine on an individual level.

It's worth noting that not everyone ties their sense of well-being to Gross Domestic Product (GDP), which serves as an indicator of a country or state's economic health. Nevertheless, the recently released data for the first quarter of 2023 indicates a decline in GDP compared to the preceding quarter. This is unsurprising given the Federal Reserve's efforts to slow down the economy. However, it is unusual for declining growth to coincide with rising consumer sentiments.

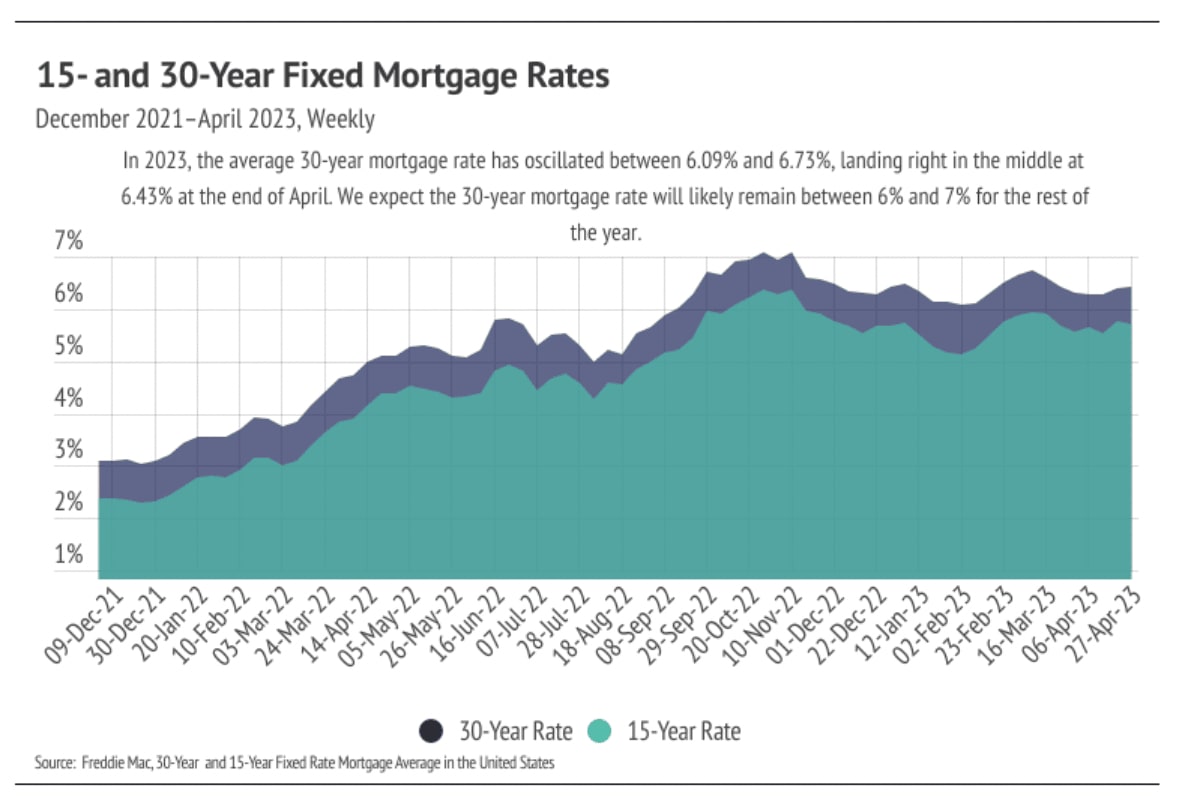

Coincidentally, the Federal Reserve held meetings right after the failures of prominent banks in March and May. In response to the inflationary pressures, the Fed chose to raise their benchmark rate by 0.25% on both occasions as part of their ongoing efforts to combat inflation. With banks tightening their credit standards after these failures, the need for further rate increases diminished. Fed Chair Jerome Powell acknowledged the possibility of not continuing rate hikes this year, although rate cuts are unlikely. As for mortgage rates, we anticipate them to hover around 6-7% for the remainder of the year.

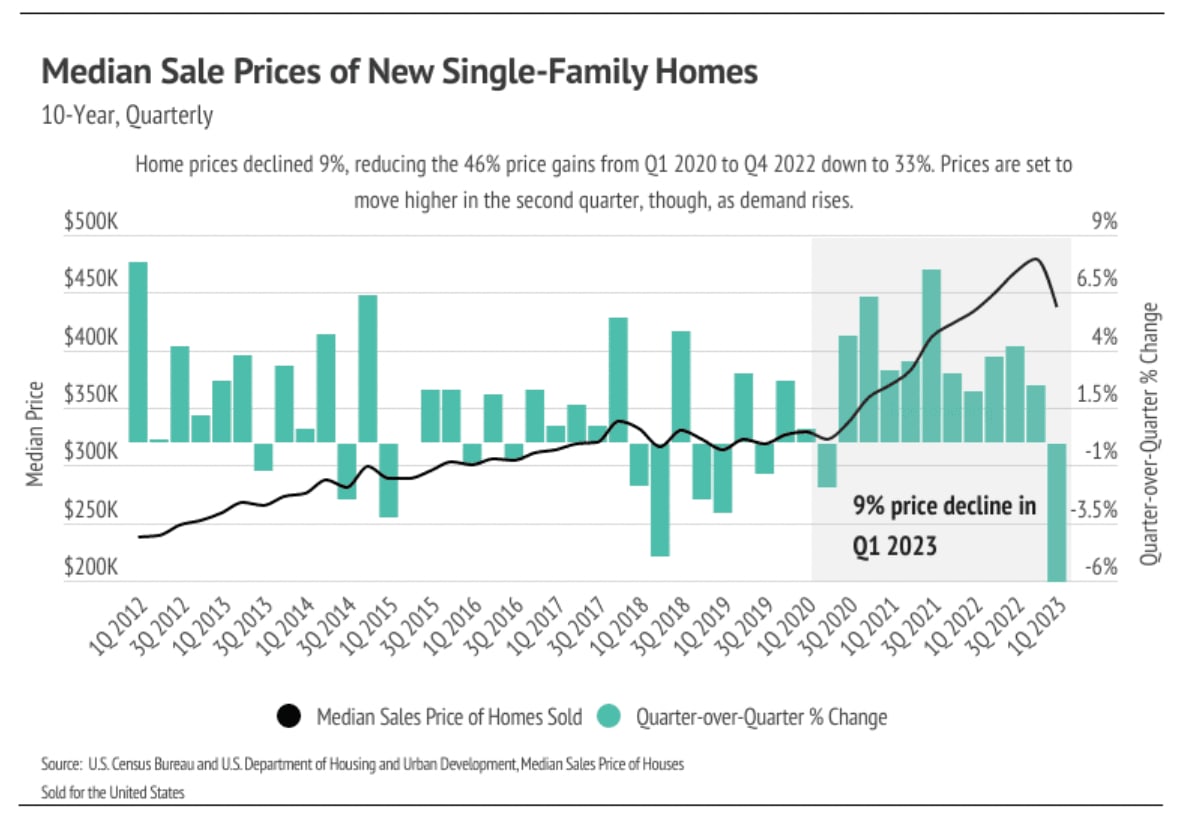

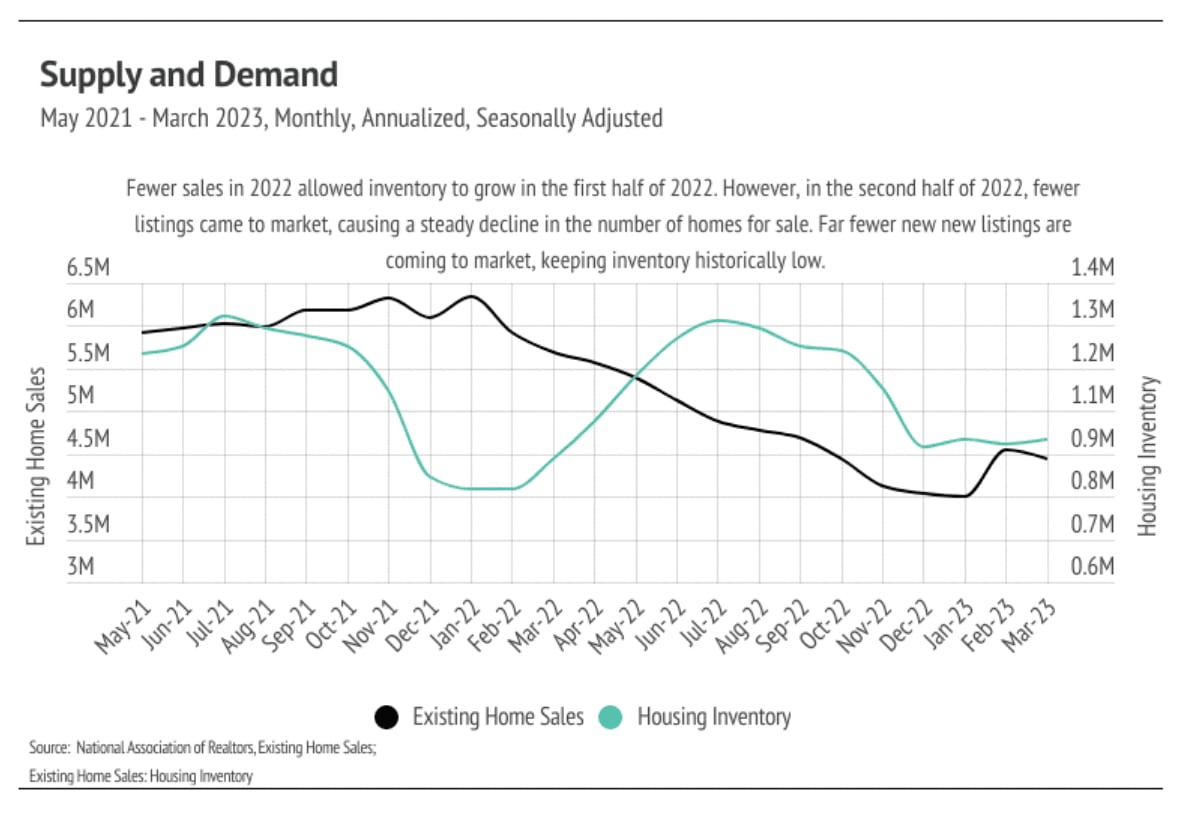

The combination of high rates and high inflation had a negative impact on consumer sentiment. Just as buyers were drawn into the market in 2020 and 2021, they found themselves priced out of the market in 2022. It is reasonable to expect fewer buyers in the market when considering the impact of rate increases alone. Moreover, after experiencing a significant number of transactions in 2021, it is natural to observe a decrease in both buyers and sellers in the following years, as most individuals do not engage in real estate transactions annually. The historically low rates made it an opportune time to buy and sell, but now the housing market must grapple with both high rates and a smaller pool of participants. The inventory remains low, primarily due to a decrease in new listings compared to the average, resulting in a limited supply of homes. Although demand has decreased on an absolute basis, it still outpaces the number of available homes.

It's important to remember that different regions and individual houses can deviate from broad national trends. For a more in-depth understanding of your local area, we have included a Local Lowdown section to provide you with tailored coverage. Generally, higher-priced regions such as the West and Northeast have been more affected by mortgage rate hikes compared to less expensive markets like the South and Midwest, primarily due to the absolute dollar cost of the rate increases. As always, we remain committed to monitoring the housing and economic markets, ensuring we provide you with the best guidance for your home-buying or selling journey.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

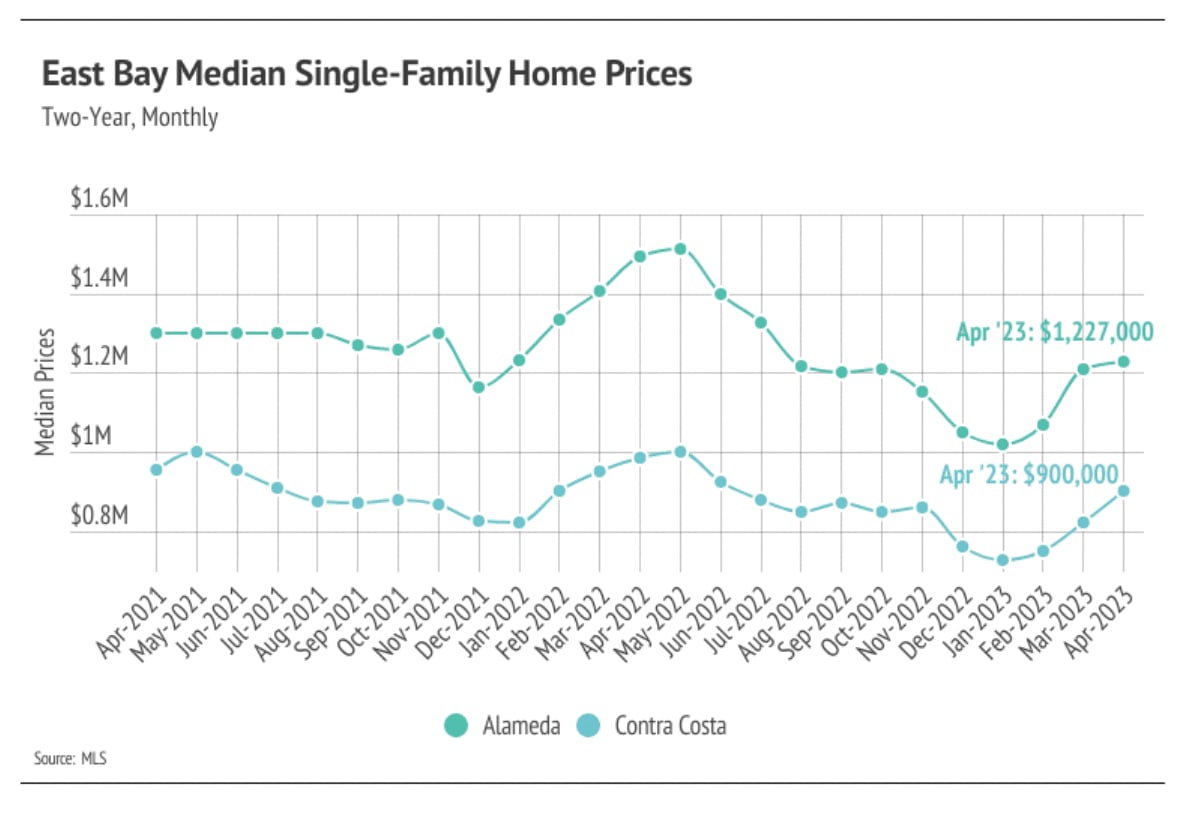

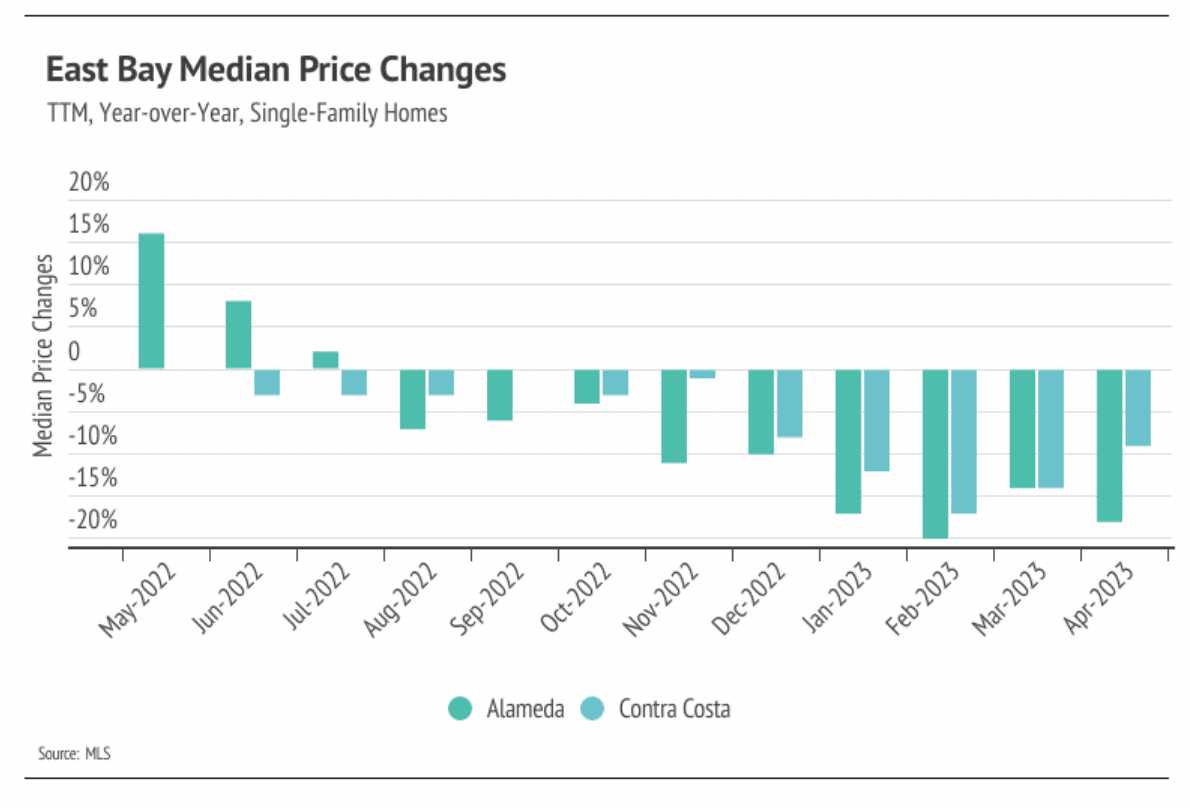

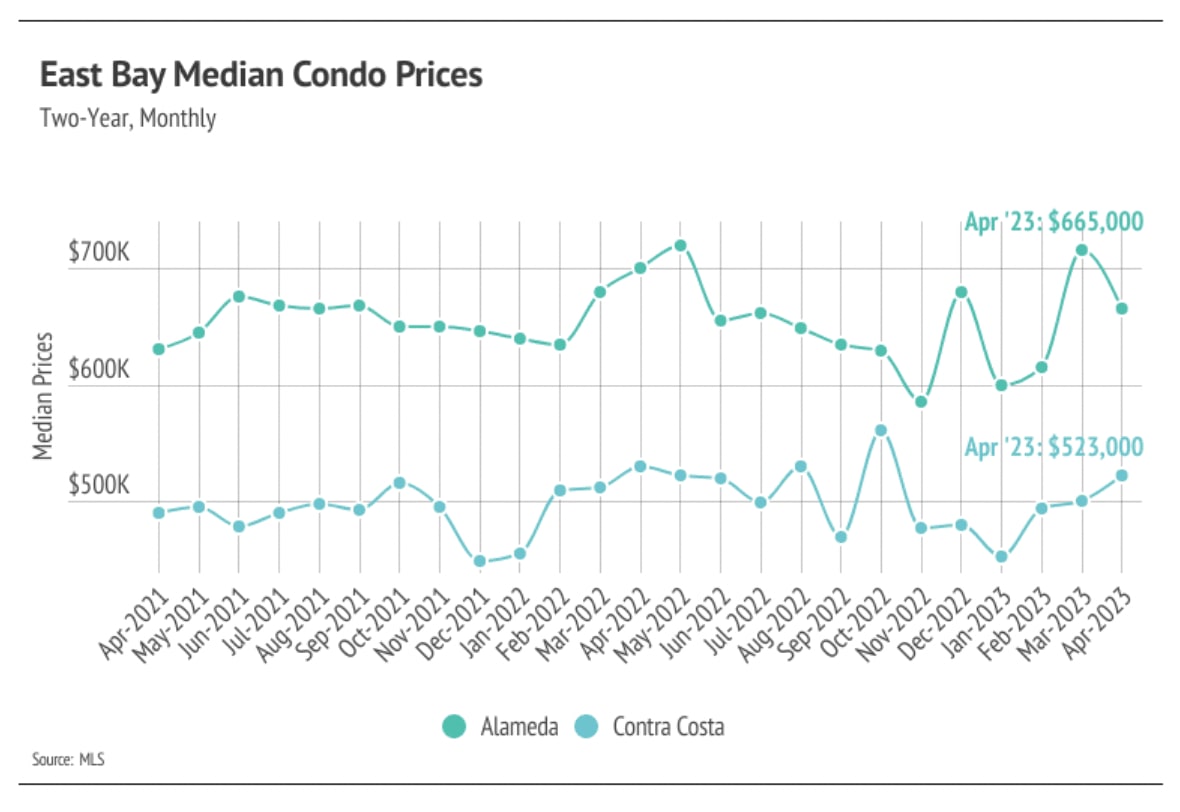

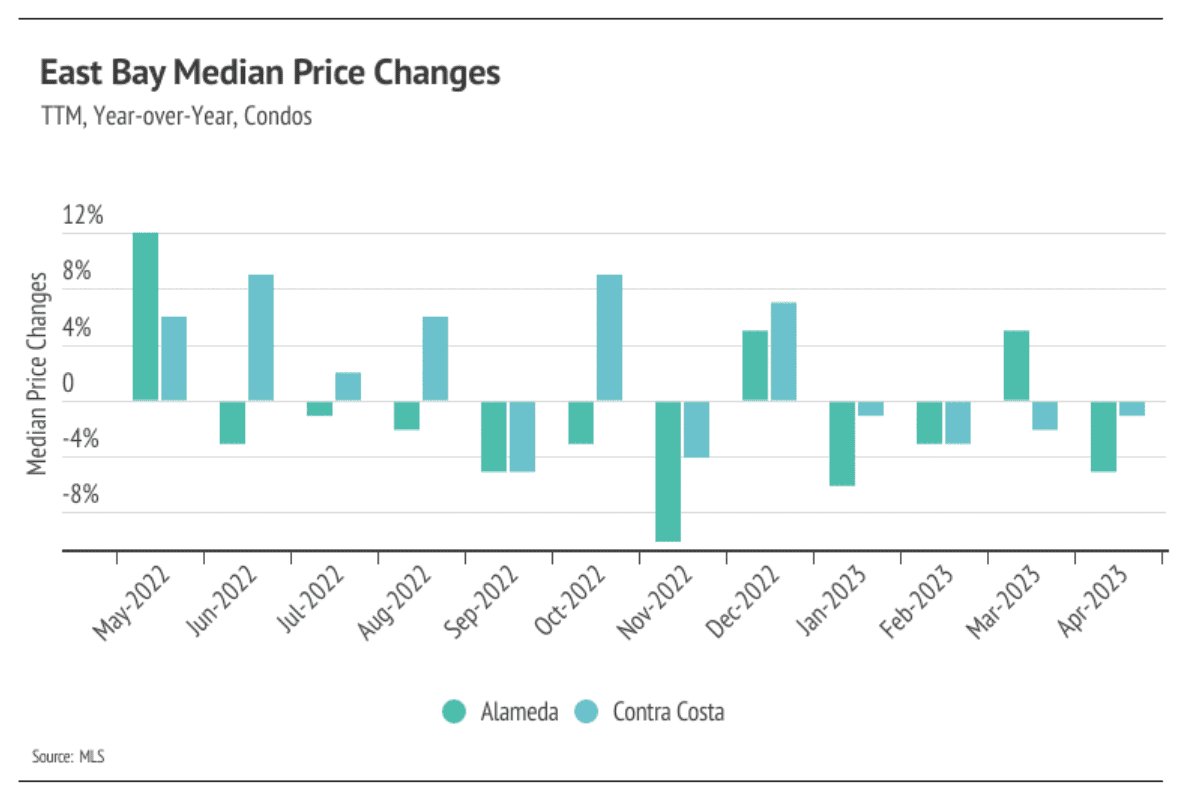

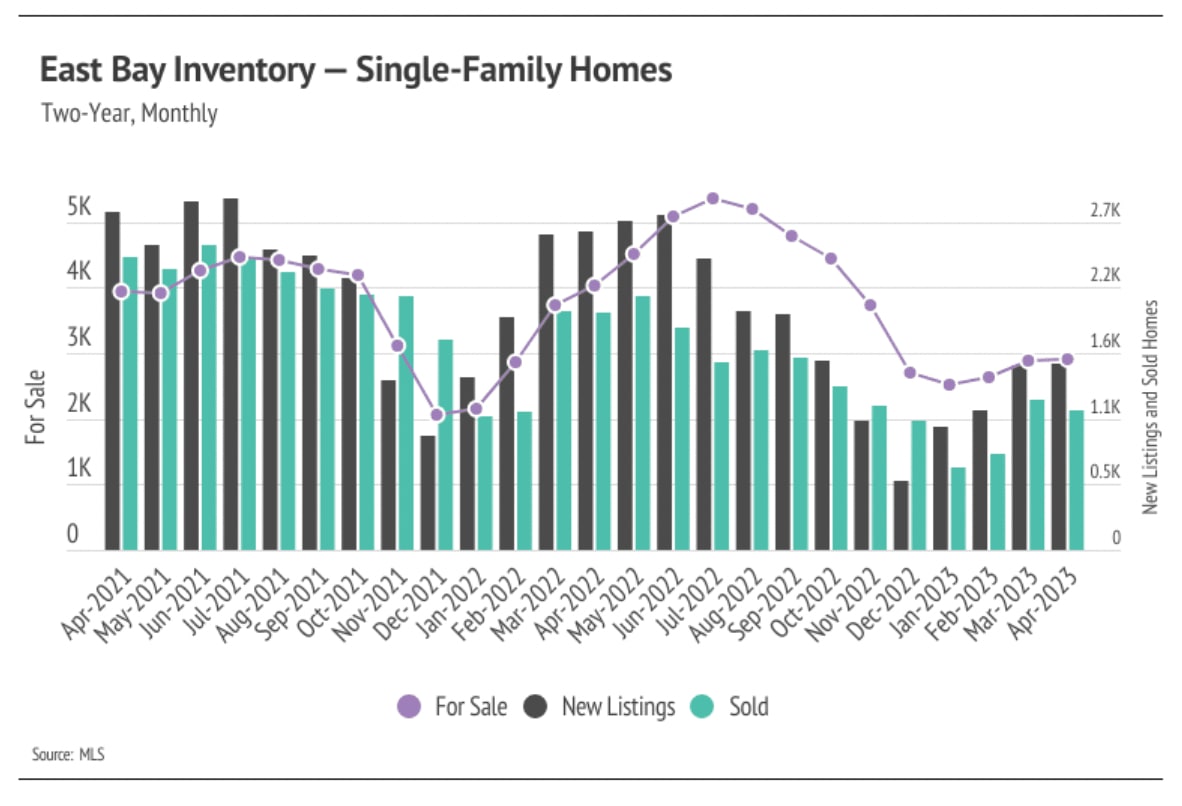

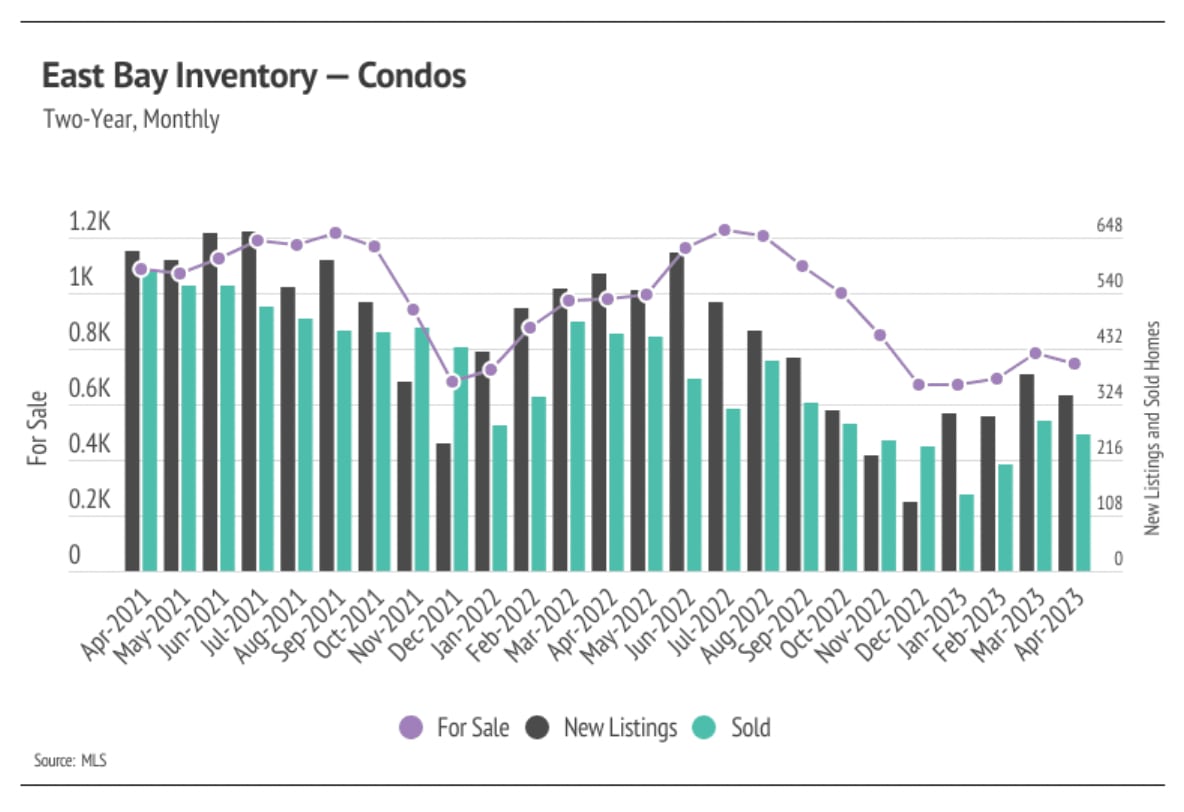

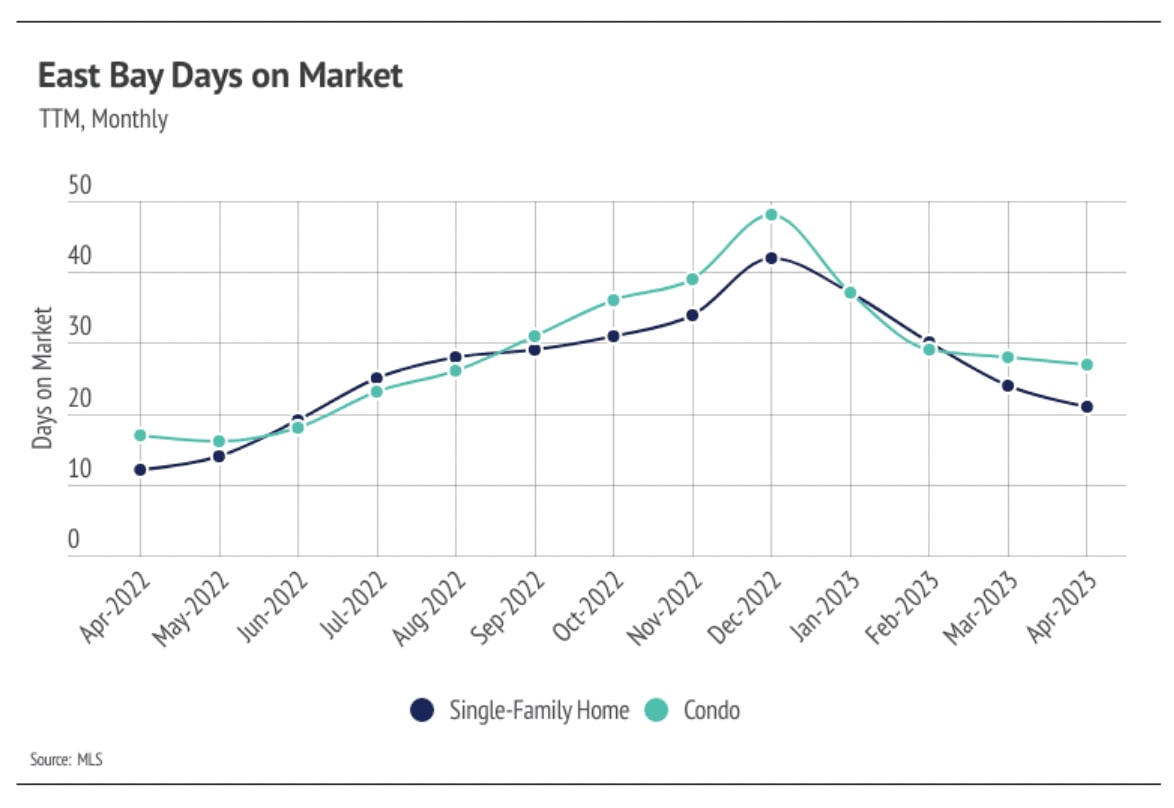

In the vibrant East Bay market of 2023, inventory has once again become a driving force behind the rapid appreciation of home prices. Last year, prices for single-family homes and condos reached their peak in May, as buyers hurried to secure mortgages at lower rates. Towards the end of 2021, the Federal Reserve announced rate hikes that would have a swift impact on rates in 2022. In the first four months of that year, the average 30-year mortgage rate surged by 2%, surpassing 5% for the first time since 2011. This sudden increase in rates led to a 27% rise in the monthly cost of financing, prompting buyers to act swiftly and enter the market.

As rates continued to climb, the market gradually cooled, and home prices adjusted to accommodate the higher mortgage costs. Both supply and demand experienced a decline in the second half of 2022, with activity falling below normal levels. However, in 2023, we witnessed a resurgence in demand despite elevated mortgage rates. Unfortunately, this increased demand has not been met with the usual number of new listings.

This year, the supply of new listings has been significantly lower than what is typically observed. Traditionally, inventory grows in the first half of the year, with new listings outpacing sales by a considerable margin. However, at this stage, the second quarter's inventory growth cannot keep up with the demand, leading to a persistently unbalanced market. As a result, the supply of homes and overall sales remain historically low throughout the year. As demand continues to rise during the summer months, competition among buyers will intensify, driving up home prices.

Condo prices are currently near their record highs, and if the trend of declining inventory persists, we could see prices reach new heights during the summer months. It's important to stay informed and be prepared for the potential challenges of a competitive market. As your trusted advisors, we will continue to closely monitor the situation, providing you with the guidance you need to navigate these conditions and make informed decisions.

In April, we observed a slight increase in single-family home inventory, while condo inventory experienced a decline. Both sales and new listings decreased compared to March. However, it's important to note that a decline in sales doesn't necessarily indicate a weakening demand. The availability of active listings influences the number of home sales. Since new listings dropped by 41% compared to the previous year, it's not surprising to see a corresponding decline in sales. Despite higher interest rates, which typically reduce the pool of potential homebuyers, the seasonal demand far outweighed the available inventory.

Over the past three months, we witnessed a remarkable 70% surge in sales, while new listings only saw a modest increase of 42%. In a typical year, the percentage change in new listings would match or even surpass the change in sales. This disparity highlights the intensifying buyer competition in the market and the limited supply of homes. As a result, sellers are gaining more negotiating power in these conditions.

To illustrate the shift in seller advantage, let's consider the numbers. In January 2023, the average seller received 95.4% of the list price, whereas in April, that figure rose to 103.3% of the list price. This indicates that sellers are achieving higher sale prices and enjoying increased leverage in negotiations.

Looking ahead, it is highly likely that inventory will remain constrained for the remainder of the year, leading to heightened competition among buyers. As we enter the summer months, the market is expected to become even more competitive. It's important for buyers and sellers to be well-prepared and work with experienced professionals to navigate these conditions successfully.

Rest assured that we are committed to providing you with personalized guidance and support as we navigate the current market dynamics together. Our goal is to help you achieve your real estate objectives while ensuring a positive and rewarding experience.

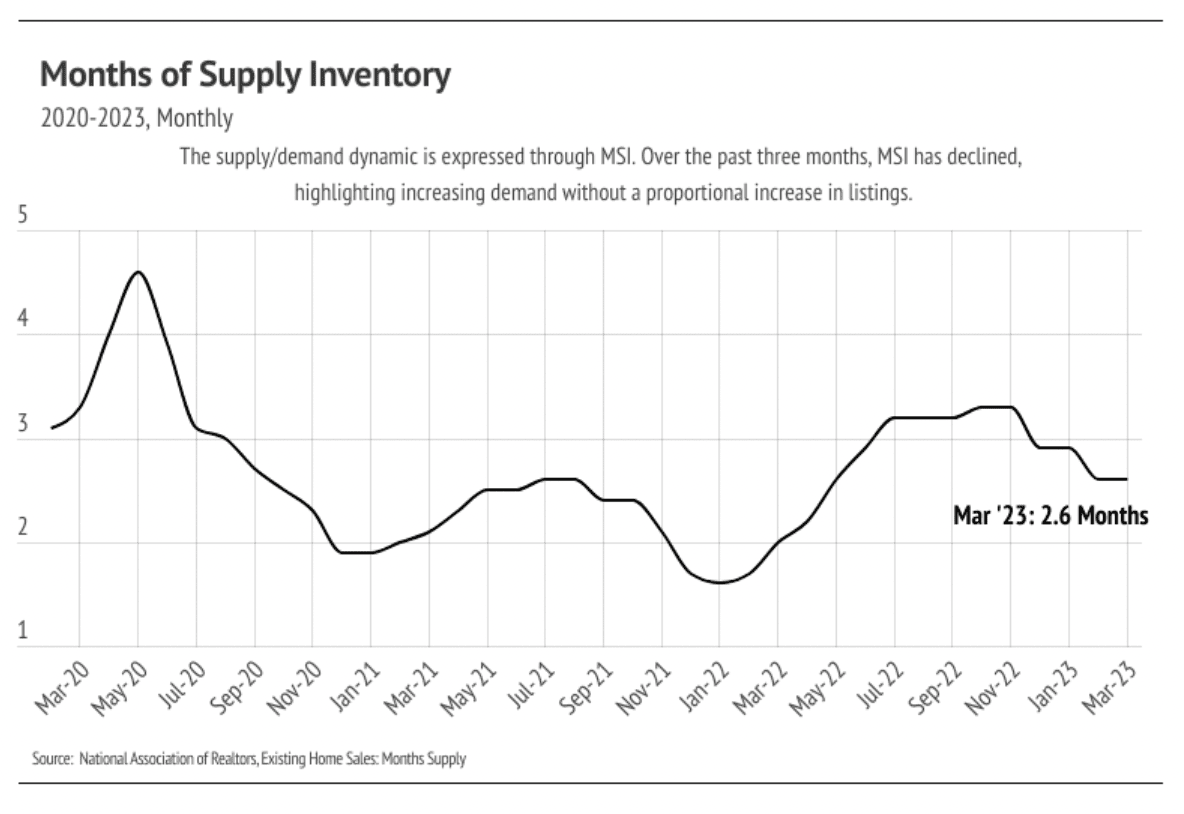

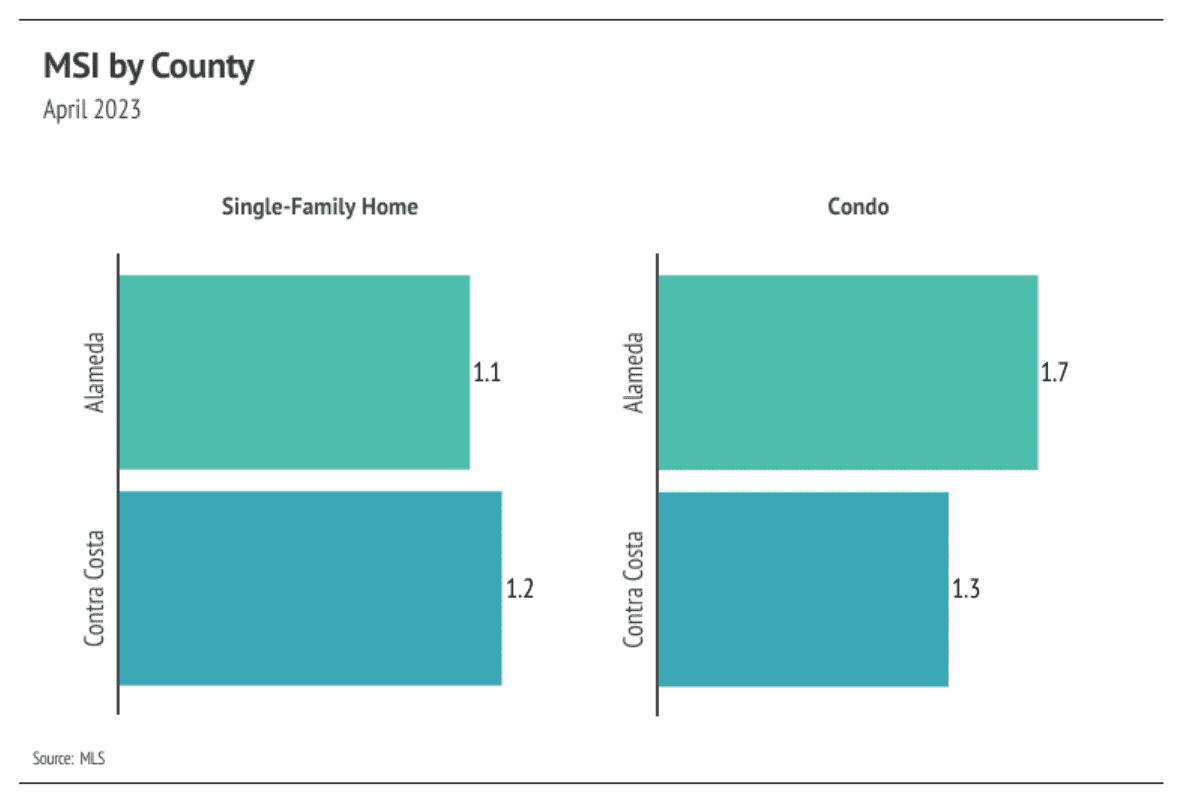

Months of Supply Inventory (MSI) is a valuable metric that helps us understand the supply and demand dynamics in the real estate market. It quantifies the relationship between supply and demand by measuring the number of months it would take to sell all the current homes listed on the market, based on the current rate of sales. In California, the long-term average MSI hovers around three months, indicating a balanced market where supply and demand are relatively equal.

When the MSI falls below three months, it suggests that there are more buyers than sellers in the market, creating a favorable environment for sellers. This scenario is commonly referred to as a sellers' market. Conversely, when the MSI surpasses three months, it indicates an abundance of sellers compared to buyers, resulting in a buyers' market.

In the East Bay market, sellers tend to enjoy favorable conditions. The recent decline in MSI for both single-family homes and condos over the past three months reinforces the increasing negotiating power of sellers. This means that there are more buyers than available properties, creating a competitive landscape in which sellers have an advantage.

Understanding the market dynamics, including the MSI, is crucial for both buyers and sellers. As experienced professionals, we are here to provide you with the insights and guidance necessary to navigate these conditions effectively. Whether you're looking to sell or buy a property, we will work closely with you to achieve your goals while ensuring a positive and successful real estate experience.

Stay up to date on the latest real estate trends.

Tips For Your Home

Market Update

Real Estate

Tips For Your Home

Real Estate

Real Estate

Real Estate

Real Estate

Real Estate

You’ve got questions and we can’t wait to answer them.